Global Oil Supply Is Being Squeezed From Two Directions at Once. Here Are the Best Energy Stocks to Buy.

A classic supply-side problem currently entangles the global oil market. The protracted conflict in Eastern Europe and the volatile, seesawing geopolitical tensions in the Middle East have squeezed global crude oil supply. Crude oil prices have been at elevated levels since February, and experts conclude that this geopolitical premium isn’t just a headline driver anymore — it’s a fundamental regime shift.

However, savvy investors will position themselves to take advantage of the unfolding situation. One of the best ways to make money is to recognize that oil companies generate significant free cash flow. In fact, investing in some of the best-known dividend-paying names in the oil and gas industry is not only an inflation hedge but also a potential path to wealth-generating opportunities.

Image source: Getty Images.

Why quality matters more than oil prices

The best players capable of navigating this environment are high-quality operators with diversified operations around the globe, with low breakeven costs, deep inventory reserves, and, most importantly, a proven commitment to return capital to shareholders. Investing in the stocks of such businesses means they are effective inflation and fuel price hedges, as they transform rising oil prices into capital appreciation and growing cash distributions.

If you are patient enough to hold on to your investment over the next few years when this new regime of elevated crude oil prices and rising inflation plays out, here are the two most attractive energy stocks to hold right now.

Compounding wealth through growing dividends and buybacks

In an uncertain geopolitical environment, ExxonMobil’s (XOM +0.97%) high-quality, cash-generative business offers both income generation and inflation protection. Essentially, the integrated oil company is an extremely disciplined allocator of capital, regardless of the projects it undertakes, meaning it has a deep inventory of structurally lower-cost, high-return projects.

Importantly, its shareholder-friendly policy means the company has increased dividends for 43 years, at an average annual rate of 5.8%. Additionally, the company is expected to complete $20 billion in share buybacks this year. Combined, shareholder distributions for 2026 at $37.2 billion are the second highest among S&P 500 companies. That alone is sufficient to hold this stock amid uncertainty.

Although historical performance is no guarantee of future outcomes, the stock has outperformed the S&P 500 and Nasdaq-100 over the past five years, both in absolute terms and after reinvesting dividends.

Today’s Change

(0.97%) $1.41

Current Price

$147.36

Key Data Points

Market Cap

Day’s Range

$147.17 – $150.00

52wk Range

$105.53 – $176.41

Volume

19M

Avg Vol

17M

Gross Margin

20.92%

Dividend Yield

2.77%

Why ExxonMobil keeps winning across market cycles

It’s not surprising ExxonMobil is a compounding wealth machine, especially during periods of macroeconomic uncertainty.

One of ExxonMobil’s biggest advantages is the sheer diversity of its energy franchise. Often seen as a boring and outdated industry, the beauty of the integrated business model shines through in adverse macroeconomic conditions.

By holding both “upstream” and “downstream” energy operations under a single umbrella, ExxonMobil protects its balance sheet by ensuring that when one part of the value chain encounters difficulties, the other frequently captures significant profits.

The low-cost engine driving future growth

During periods of high oil prices, Exxon’s advantage in having among the industry’s lowest breakeven costs becomes clear. Last year, management announced a goal to lower overall breakeven costs to $35 per barrel by 2027 and to $30 by 2030.

The company’s massive Yellowtail oilfield off the coast of Guyana has breakeven costs as low as $25 per barrel, which is far below the global average and roughly half the onshore breakeven costs of the average U.S. shale play.

Onshore, ExxonMobil’s $60 billion acquisition of Pioneer Resources in 2023 ensured the company doubled its footprint in the Permian Basin, which accounts for nearly 40% of U.S. shale oil production, thanks to its “stacked geology” formation where overlapping oil-rich layers stack up vertically for thousands of feet. The result is an inventory acreage with the lowest breakeven costs among shale plays.

Today’s Change

(1.92%) $3.52

Current Price

$187.38

Key Data Points

Market Cap

Day’s Range

$185.50 – $188.15

52wk Range

$146.49 – $214.71

Volume

340.8K

Avg Vol

9.5M

Gross Margin

15.15%

Dividend Yield

3.73%

A high-yield dividend play for reliable passive wealth creation

Another integrated oil company, Chevron, (CVX +1.92%) too, built its reputation through its decades-long commitment to rewarding shareholders. The stock’s dividend yield of 3.75% is higher than ExxonMobil’s.

So if you’re looking to prioritize immediate dividend payments over longer-term capital appreciation, then Chevron’s dividend should appeal to you.

Like its larger counterpart, Chevron also focuses on low-cost projects around the world, and its pending acquisition of Hess underscores its focus on obtaining low-cost assets, notably the same ultra-low-cost Yellowtail offshore oilfield off Guyana.

With similar return profiles over the years, Chevron has a more aggressive dividend payout policy than ExxonMobil, resulting in lower free cash flow. Still, the company maintains a fortress balance sheet and has paid out dividends for 39 years. Over the last five years, the stock has outperformed the S&P 500 as the company moved away from pursuing multiple expensive projects simultaneously.

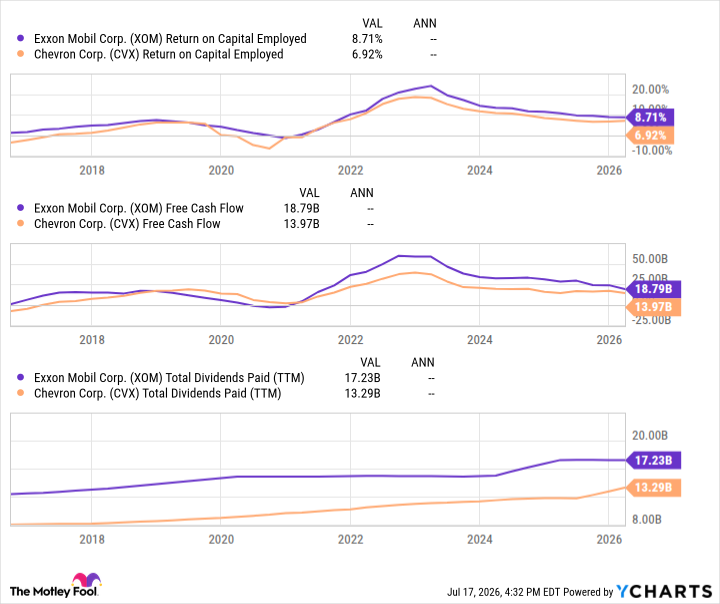

XOM Return on Capital Employed data by YCharts

For years, Chevron invested billions of dollars into the Tengiz expansion in Kazakhstan and deepwater projects in the Gulf of Mexico. Now it’s reaping the benefits. Like ExxonMobil, Chevron remains an excellent long-term pick and a hedge against rising crude oil prices.

If you are looking for a larger dividend check, Chevron is a good fit for you. If, however, you are not too bothered about receiving a higher dividend and instead look for capital appreciation over the longer term, then ExxonMobil fits the bill.