Could the UK Housing Market Become More Affordable?

This is the traditional view of the UK housing market. House prices soaring. You can’t go wrong with housing. But now the housing market increasingly works only for those whose parents are already on the ladder.

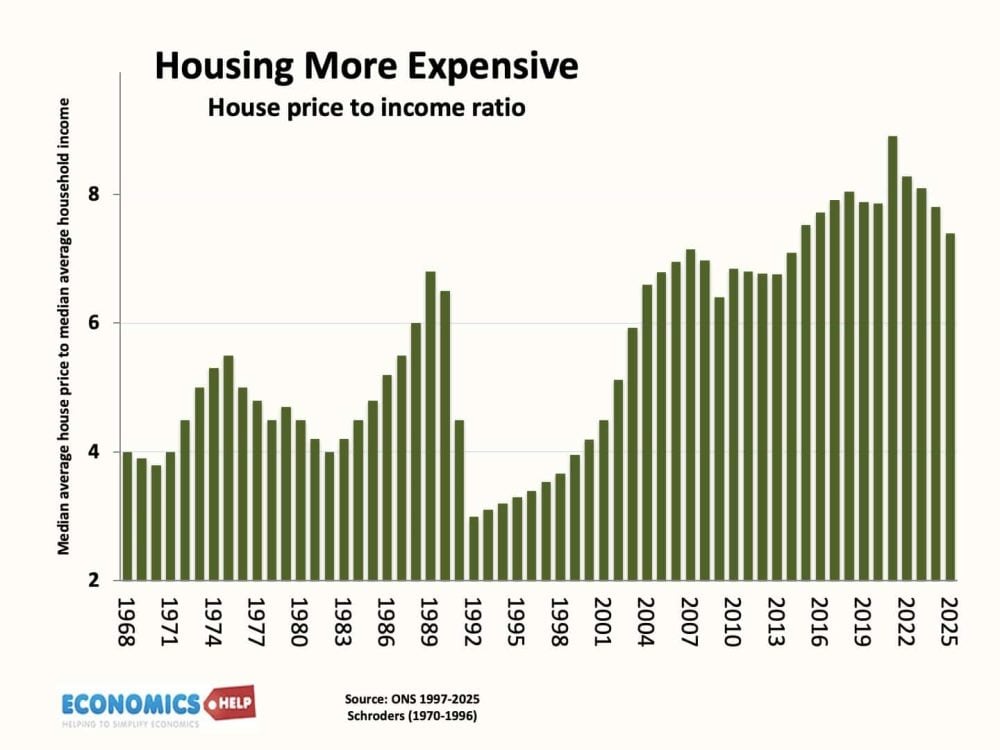

Back in 1980, houses were 4 times income; today, it is closer to seven times income. Even when prices rise, we are willing to pay the higher prices, because the alternative is paying a fortune for market rent. And it’s more than economics. It’s deeply embedded in the national psyche. An Englishman’s home is his castle, though admittedly a very small castle, the UK has some of the smallest houses in the developed world. But all this talk of a home-owning democracy is a painful reminder for the younger generation who see a ladder pulled up behind them. For decades, home ownership rates rose, but as house prices reached record levels, it was finally too much and young people were squeezed out.

Wealth

The UK currently has over £8 trillion invested in housing, which does little to boost productivity or living standards. Though it is profitable for banks a £500,000 mortgage at today’s rates will cost £900,000 over 25 years.

Despite recent modest falls, the price to income have increased in the long-term. And that is only part of the story. Young graduates now face a triple challenge: student debt, high rents and record deposits. The average first-time buyer deposit is around £61,000 nationally and well over £100,000 in London. For those who do scrimp and save, or more likely receive help from parents, they may be able to buy. This is the big change in UK property. Increasingly, the route into home ownership is not higher earnings but family wealth. The Bank of Mum and Dad has become one of Britain’s largest mortgage lenders. Over the next twenty years, trillions of pounds of housing wealth will be inherited. The risk is that home ownership becomes less dependent on work and saving and more dependent on whether your parents owned property.

Traditionally, buyers climbed a housing ladder. But today the first rung is breaking. Flats have lagged behind the rest of the market, and in the capital, most flats are being sold for less than what they were bought for, even 10, 15 years ago. Last year, average house prices stagnated, the price of flats fell 6.7%. The problem with flats is a rise in service charges, concerns over leaseholds and post-covid just a changing preference for houses with more space. But, whatever the reason, those who bought a flat are being left behind.

But the real problem is that for many, buying anything is out of the question, and that leaves them in a private rented sector, where rents have risen faster than inflation. It raises a catch 22 situation. Rents are so expensive, you want to buy, but because rents are so expensive, it’s hard to save up for deposit.

Interest rate link

In the 2010s, cheap money inflated prices. However, since 2022, higher interest rates have reduced that support. And The Bank of England warn that rising oil prices combined with relatively high inflation expectations, risk further rises to interest rates.

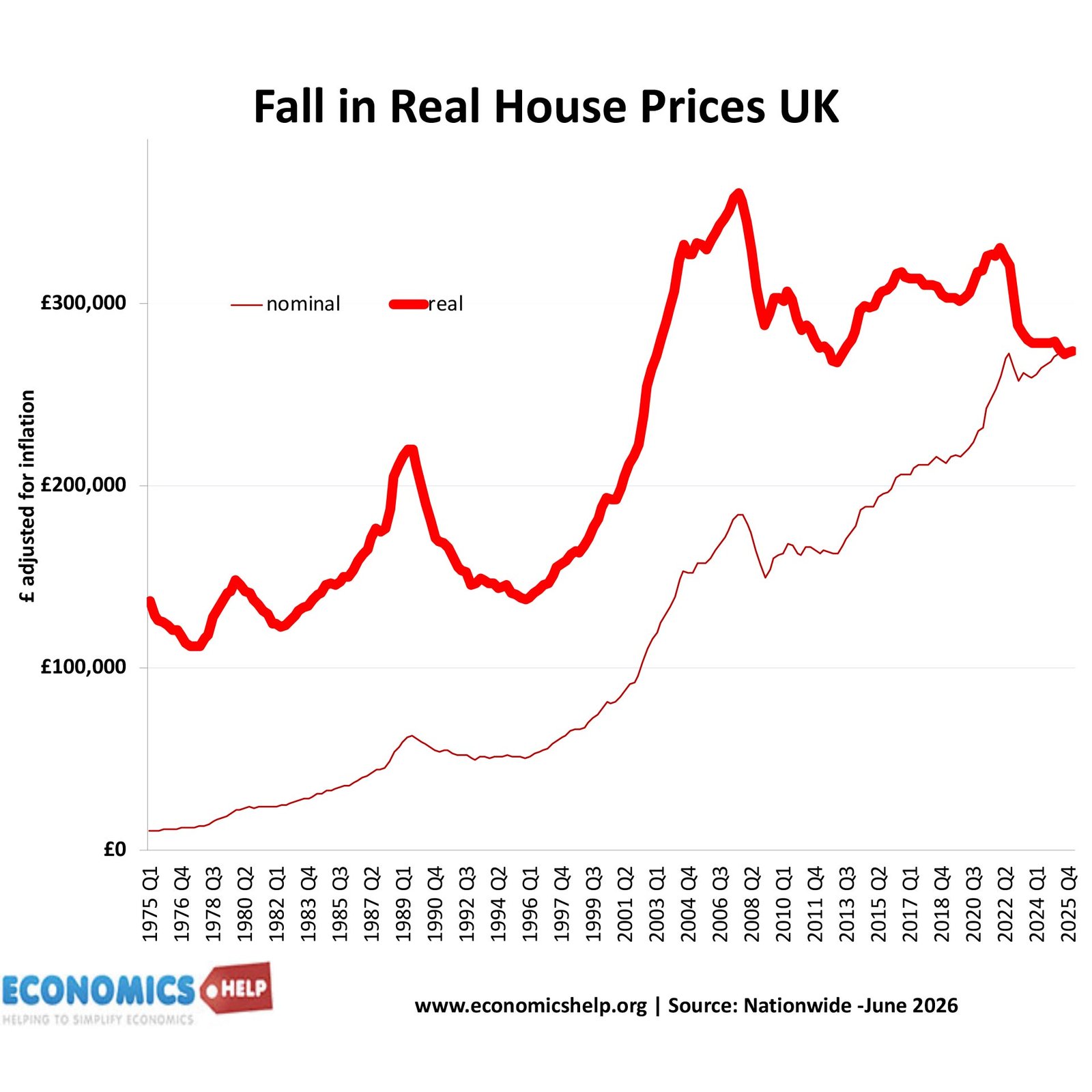

Nominal prices grab headlines, but inflation-adjusted prices tell a different story. In real terms, UK house prices are below their 2007 peak and have fallen significantly since 2022.

Poor income growth

This has slightly improved housing affordability. But less than you might imagine, real income growth has been very poor since the financial crash of 2007, and forecasts suggests there is little if any income growth to come. In addition, the FT report that although there has been some improvement in house price to income ratios, for actual first time buyers, it is less promising.

Supply

Given high house prices and the fact the the UK has a low volume of housing stock compared to other countries, the perennial question is why not build more. Successive governments have announced ambitious targets. Yet, in practise, they fail to get anywhere close.

The housing shortage is real. Yet solving it is harder than simply approving more planning applications. Construction costs, labour shortages, expensive land and tighter safety regulations all limit how quickly supply can expand. In the last 3 years only 50% of planning permissions ever make it to construction. If the average cost of building a three-bedroom semi is around £282,000, it is difficult to see how developers can produce genuinely affordable homes.

Back in 1980, when house prices were cheaper the UK had a much bigger stock of council housing, which provided subsidised rents. In the post-war period, the UK solved a real housing crisis by building factory-produced pre-fabs at low cost. By the 60s, and 70s, councils were building at large scale and at relatively low cost. This led to a big rise in supply.

But, when they were sold off from early 1980s, councils also stopped building and have lost the capacity to build at scale. This is often pointed out as a turning point for the UK housing market. However, it can’t be the only explanation, the UK still has one of the highest ratios of social housing, even after so many have been sold off. One solution is a national council building scheme but, JLL stated two years ago it would cost at least £205 billion to build housing for every household on a waiting list. Even if you got the Bank of England to print £200 billion of cash, it doesn’t solve the UK’s shortage of builders, materials and land for building.

And as supply is constrained, the rise in the population has led to higher number of households, which is a factor in propping up demand. More than anything the UK housing construction sector needs to find a way to reduce prices. In many ways, we are still building homes with 1930s construction methods but 2020s wages and regulations.

Britain suffers not only from a shortage of homes but from a mismatch in how housing is used. Many older households occupy large family homes while younger families struggle to find space. But there is no incentive to downsize, cash savings would be used to fund social care, wealth tied up in housing is protected. It’s very inefficient, but the UK tax system rewards staying in your house and using it as a store of wealth It’s certainly very expensive and time consuming to move. The observer compares different attitudes to downsizing.

But, for all the talk of unaffordability, could we be starting to see a gradual fall in house prices? Certainly adjusted for inflation, we are seeing lower prices, and there are reasons to see more of this.

Firstly, in the 2010s, quantitative easing saw £900 billion of newly created money. This lowered interest rates and increased asset prices. But now the Bank of England is reversing this scheme, this pushes up in interest rates and is likely to have downward pressure on asset prices. Certainly, the reversal of QE corresponds to falling real prices. Secondly, there is a changing attitude to housing market. It’s no longer seen as a place to see capital gains. In recent years, you would have been better off investing in gold or stock market. Thirdly, since 2016, there has been a steady change in tax and regulation which has led to decline in buy to let investor market. According to Savills 700 rental homes are listed for sale every day, up 28pc in two years.

Also, against a backdrop of a worsening economic outlook, demand has plummeted in recent years. A combination of rising interest rates, uncertainty and slow economic growth. At the start of the year, modest price rises were forecast, but the Iran crisis has led to a downgrade of forecasts. If disruption to shipping through the Strait of Hormuz persists, the prospect of higher inflation and higher interest rates will weigh further on the housing market. For many years, the UK saw real house prices growth that exceeded that of most other G7 countries, but now the UK could be looking at a sustained period of falling real house prices. Even past forecasts of rapid population growth look shaky, fertility rates are falling and net migration has come down; certainly, in terms of rental growth, the population change has impact on prices. If you believe house prices never fall, don’t forget Japan shows that house prices do not always rise forever, particularly when demographics weaken and economic growth slows.

The housing market is no longer the one-way bet it once appeared to be. Higher interest rates, weaker demographics and an end to the speculative fever of the 90s and 2000s could mean years of stagnant or falling real prices. But even if prices cool, affordability may not improve dramatically.

The deeper issue is that Britain increasingly allocates housing through accumulated wealth rather than earned income. Until that changes, the dream of a home-owning democracy will remain out of reach for many younger households.

Sources

https://ww3.rics.org/uk/en/modus/built-environment/homes-and-communities/uk-housing-shortage.html

https://www.socialhousing.co.uk/news/jll-estimates-205bn-cost-to-clear-housing-waiting-lists-and-calls-for-end-of-right-to-buy-86953

https://www.zoopla.co.uk/research/

https://observer.co.uk/news/business/article/downsizing-isnt-yet-in-richards-interest-that-needs-to-change

https://www.telegraph.co.uk/gift/3242a519bc70376a

https://ww3.rics.org/uk/en/modus/built-environment/homes-and-communities/uk-housing-shortage.html