Do a Roth Conversion at a Discount

|

|

<!–

Roth conversions are the process whereby one pre-pays taxes on a tax-deferred retirement account so they can never pay taxes on that money or its earnings ever again. They can be part of a wise financial plan, although the decision about whether to do them is perhaps the most complicated in personal finance.

But what if you could do that Roth conversion at a discount, i.e., pay less in tax than you would expect to accomplish the same thing? Would it be a more attractive play to you? Would you be more willing to do one? Or to do more frequent or larger conversions? Probably. Well, there are two ways to do a Roth conversion “at a discount.”

Method #1 — Do Roth Conversions During Bear Markets

One method of doing a Roth conversion “at a discount” is to wait until the value of your portfolio falls, typically in a nasty bear market. It can be particularly fruitful to do this in a year like 2022 when both stocks and bonds fall, especially if you manage to time the transaction close to the very bottom of the bear.

Imagine your portfolio falls in value by 25%. A $2 million portfolio becomes a $1.5 million portfolio. Maybe you had an IRA that was $300,000 before the drop. Now, it’s $225,000. If you convert the entire IRA at 37%, what would have cost $300,000 * 37% = $111,000 in federal income taxes now only costs $83,250. That’s a $27,750 “discount.” In some cases, the discount will be even more significant. Imagine a situation where half of a Roth conversion would be done at 32% and half at 24%. If the market falls, maybe the entire Roth conversion can now be done at 24%.

This all, of course, assumes the same long-term outcome for those stocks and that you can somehow time the Roth conversion well, neither of which is entirely true. It also assumes the money you are using to pay the taxes on the conversion did not also just take a haircut. But even getting a 5% discount is better than no discount, assuming the Roth conversion otherwise makes sense.

More information here:

- Get Rich Fast as a Millionaire with Roth Conversions

- Roth vs. Tax-Deferred: The Critical Concept of Filling the Tax Brackets

Method #2 — Get an Illiquidity Valuation Discount on the Asset in the IRA

A more powerful method is to use illiquidity to your advantage. An illiquid asset is not as valuable as one that is liquid. However, if the liquidity doesn’t matter to you, then this is a great way to get a discount on a Roth conversion. It basically works like this. Take a privately held investment that is worth $100,000. Put it in a traditional IRA, probably a self-directed IRA. Then, move it to a Roth IRA. In order to do this and calculate the appropriate tax bill for the conversion, you’ll need to assign a value to it at the time of the conversion. You might even have to pay for an appraisal. But appraisals take illiquidity into account.

If you paid $100,000 for the investment and expect to sell it for $200,000 but not for seven years, what is it really worth today?

Fair market value discounting is an accounting technique where you adjust the value of an asset/investment for multiple factors including:

- Minority interests (lack of control)

- Lack of marketability (illiquidity)

- Fractional interests (difficult for a prospective purchaser to buy the whole thing)

Private investments, unlike publicly held stocks and mutual funds, are subject to valuation adjustments. This includes real estate, partnership interests, and small businesses like the one behind this blog. When valuing these assets for a Roth conversion or to move them into a trust, their value is naturally discounted by an independent third party. Their well-supported appraisal can justify the discounts to the IRS. IRA custodians are required to report the fair market value of IRA accounts annually, both to you and to the IRS. Proper documentation is obviously key. The appraisal isn’t free, but if you have to do it anyway to report to the IRS annually, why not also use it for a Roth conversion?

Note that putting your small business into your own IRA probably isn’t going to fly with the IRS due to self-dealing rules. But a minority interest in someone else’s small business often works just fine in an IRA. See Peter Thiel for details.

|

|

<!–

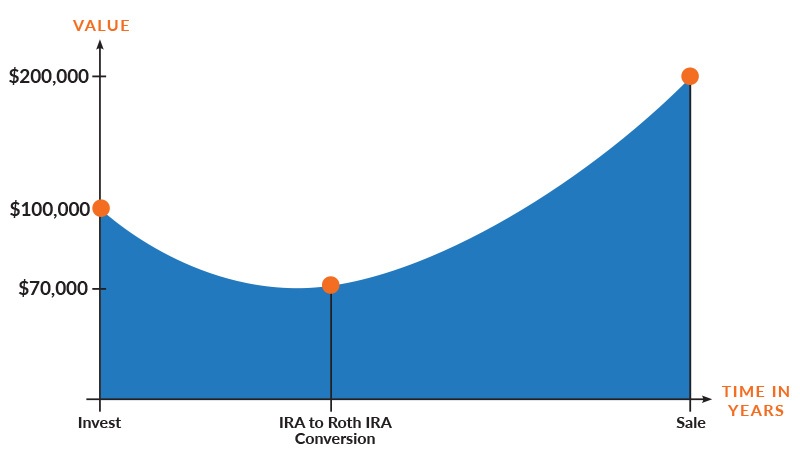

The Ideal Investment for a Discounted Roth Conversion

Ideally, you want the investment to have great long-term returns but terrible short-term returns. You want a “J-shaped” investment curve. That way, you can buy the investment at $100,000, convert it at $70,000, and then sell it years later for $200,000.

Of course, when you put an investment like equity real estate in an IRA, you lose out on the depreciation provided by that investment. One can argue that the tax advantages provided by the retirement account still outweigh those provided by depreciation, but many real estate investors just choose to put their stocks, bonds, and mutual funds in their IRAs and use taxable funds to buy real estate. When you consider the additional value of a discounted Roth conversion, however, it might be worth the significant additional hassle of putting the real estate into the IRA.

More information here:

- Roth Conversions for a Smarter Retirement

- Why Wealthy Charitable People Should Not Do Roth Conversions

How Big Can These Discounts Be?

You might be surprised how big these discounts can get, especially if you have more than one of them. While I don’t pretend to be an accountant (and don’t ask me to calculate these), here are some typical ranges:

- Illiquidity: 10%-40% discount due to the inability or challenge of selling an asset quickly at a fair market value. This is very common in small businesses and partnership interests.

- Lack of control: 10%-35% discount due to the inability to control the investment. This is very common in limited partnerships and LLCs such as those used to invest in private, passive real estate. It can be demonstrated by limited access to financial information, restricted voting rights, or a lack of say in major business decisions.

- Minority interest: 15%-35% discount due to their inability to influence operations and distributions. This is common in small businesses, partnerships, private corporations, and LLCs.

Add up all those discounts, and it can be substantial. For example, a 25% illiquidity discount + a 15% lack of control discount plus a 20% minority interest discount is a total of 60% off. Even if you have to multiply the discounts together, which I suspect is the proper way that a real accountant would do this, it totals to a (.75*.85*.8) = 49% discount. Paying half as much in tax makes a Roth conversion dramatically more attractive. Not to confuse the subject, but using this sort of valuation discount when moving an asset into an irrevocable trust also dramatically reduces the amount of estate tax exemption you must use to do so, reducing future estate taxes.

Sometimes, illiquidity and lack of control can be your friend. One of those times is when valuing otherwise excellent investments to do a Roth conversion.

What do you think? Have you ever done a discounted Roth conversion? What happened?

The post Do a Roth Conversion at a Discount appeared first on The White Coat Investor – Investing & Personal Finance for Doctors.

|

|

<!–