Rising Bond Yields – What is Cause?

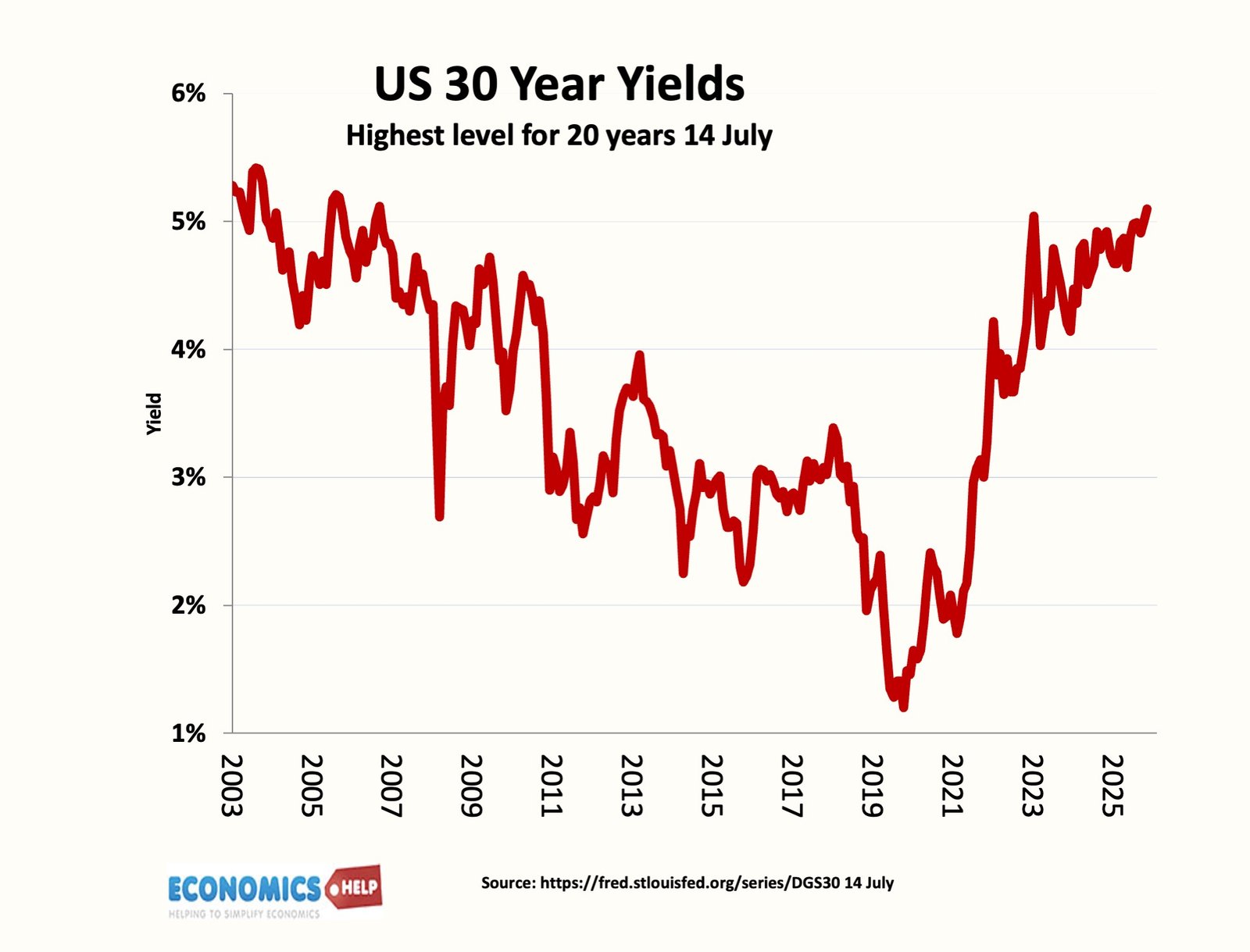

Last Thursday the US government tried to borrow money. But investors would only take the supposedly risk free 30 year Treasury at just over 5%, the highest 30 year yield since before the financial crisis. But the difference is that in 2008, US debt was 39% of GDP, today it is 100%. And the rise in bond yields and debt at the same time has a major consequence, the US is forecast to spend over $1 trillion on debt interest payments this year alone, a figure that could rise to $1.6 trillion in 10 years’ time. To put that figure in context interest payments are larger than defence, homeland security, education, and roughly neck and neck with Medicare spending. So are rising bond yields signs of impending fiscal doom, higher inflation or simply a loss in investor confidence?

Firstly, it is not a US phenomenon, we have bond yields rising across the world, notably Japan.

As recently as 2020, investors paid the Japanese government to borrow their money, negative yields, now 30 year Japan bond yields are soaring. What changed in Japan is a really interesting story. On the positive side, Japan’s rising bond yields partly reflect the end of deflation and return of inflation. For many years, Japan actually wanted to end its deflation, but now inflation is coming back, though unsurprisingly there is now a worry that you can have too much of a good thing.

But, it is more than inflation, the real Japanese yield has increased from – 0.3% in 2023 to 0.5% today. Japan has the largest public sector debt in the world, so a rise in Japanese bond yields has big impact. Not least, with higher Japanese bonds, there is incentive to bring back Japanese investment in from the US. Markets are interlinked, Japan has one trillion in US bonds. So rising Japanese yields will affect US yields too. If Japan sells US treasuries, it puts upward pressure on US bonds. The US hasn’t exactly fallen over themselves to attract foreign buyers. The truth is there is a global rise in debt issuance and countries who rely on external funding, like the UK, France and the US will face much greater competition and therefore rising bond yields.

Inflationary pressures

But, in the short-term, it is the ongoing conflict in Hormuz that has restarted fears of higher oil, petrol and inflation prices. US CPI Inflation is at a three year high, and it is this that is driving higher bond yields. By, the way it is not just rising oil prices threatening inflation. We have seen AI cause a surge in price of memory chips and semi-conductors. AI data centres are starting to see a rise in US electricity prices, there may be more to come. The global El-Nino effect is also pushing up food prices, with analysts warning of £6.50 for a flat white. Possibly a greater economic crisis than 6% bond yields.

But all these inflationary pressures mean that Central Banks have flipped. At the start of the year, there was expectation of lower rates, now there is expectation of higher rates, and this is a big driver in boosting bond yields.

However, whilst cyclical factors can explain a large part of the movements in bond yields, we shouldn’t forget the underlying long-term trends. For most governments, debt is expected to rise for three reason. Across the developed world, we see a fall in the working age population and rise in old age dependency. This means a higher share of GDP will go to mandatory government spending programmes like pensions and health care. In the UK, the OBR showed how fiscal transfers depend very much on age. In this regard, Japan was the canary in the coal mine, with the working age population peaking in 1995. An ageing population doesn’t just increase government spending but tends to slow down economic growth rates. You can see growth rates falling in the OECD.

In the fact, the US has had one of the best performing growth rates, but the very high debt of the 1940s was steadily eroded by the post-war boom. The US now faces debt rising, but slower economic growth. A key metric is considered to be when debt interest payments as a share of GDP are higher than economic growth. You can see that for the first time in 30 years debt interest payments have overtaken growth.

But the difference with the early 1990s, is that unlike the 90s, today the outlook is for lower growth and higher deficits. This is the doom loop of debt higher yields → bigger interest bill → bigger deficit → more bond issuance → higher yields. The US deficit is really very high for the stage of the economic cycle.

When you see graphs like this for the UK or US, it is important to stress, this is not a forecast, but projection on current policy. If you adjust spending or tax, this becomes manageable, but in an era of political populism, there are little incentives or willingness to make painful choices which put spending on more sustainable path. Because of this investors are looking at a term premium, in plain English this means investors want extra payment for lending for a long-term when they don’t trust the outlook.

In France, the government raised retirement age from 62 to 64, but it was very unpopular and the National Rally, leading in the polls promise to take it back down to 62. France spends about 14% of GDP on pensions, the third highest in the OECD, and pensions makes up about a quarter of France’s budget with average payments around €1,500 compared to £1,000 in UK. French bond yields are rising partly because of this backdrop, the country can’t pass pension reforms without mass protest, and the fiscal credibility of the political system is very weak.

The other problem is that even these scary outlooks for debt assume there will be no further economic shock, but now everyone kind of expects economic shocks. Tariffs, oil prices, global conflict, energy disruption, Covid, have all caused unexpected fiscal shocks and a slowdown of economic growth.

What does it mean?

So what does it mean if bond yields go up? Well for investors and those with pension funds, it means higher interest payments and higher annual income. So some will benefit from higher bond yields. But there are fewer positive aspects. Primarily it means higher debt interest payments which crowd out public services, rising debt payments accounts for much of the recent increases in tax. Thirdly, a rise in bond yields, generally corresponds to lower demand for stocks. If you can get 5% from bonds, it is more attractive than stock market. Higher bond yields, also reflect higher interest rates in the economy, that means more expensive mortgage rates and less disposable income.

From a historical perspective, bond yields are much lower than 1970s, 80s and 90s, a period of really quite high bond yields. The difference is that in the 1970s, government debt was lower and growth rates higher.

So the big question, should we be panicking or is it all fine? Well there is definitely a soft-landing scenario. Iran de-escalates, inflation fades. Although, we’ve kind of been hoping for that since early March. Also, you could argue we are just returning to a pre 2008 normality, 5% bond yields are fairly standard by post-war period. The problem is the combination of low growth, rising debt, ageing population, external shocks and inflation all at the same time. It is a headache, which will increasingly manifest in the future.